Guest post by Mike Lewis

One of this blog’s foundational themes is that economic facts don’t mean much without an analysis of power. At the same time, over the last fifteen years I’ve watched big NGOs develop specific ways to wield economic facts, perhaps even to fetishise them, as a way of influencing power. With the new government favouring a similar “numberism” , it seems a good moment to consider this technique’s challenges.

Consider the first speech of the UK’s new Chancellor on 8 July. Light on policy content, but with guaranteed cut-through thanks to a mega-number: £140 billion, the GDP “foregone” by the UK economy not growing as fast, on average, as OECD economies over the last 14 years. Plus a side-serving of fiscal black hole: £58 billion of resulting “missing” tax revenues.

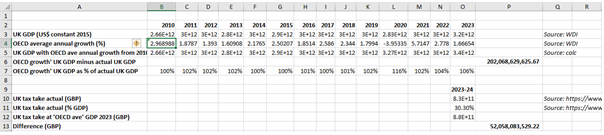

It’s obvious how the £140/58bn figures are calculated: OECD growth figures from the World Bank or another sources, applied to 2010 UK GDP, then 2023 UK GDP subtracted. Then multiply this ‘foregone’ GDP to the UK’s tax take/GDP ratio. It takes about 90 seconds with a spreadsheet…something like this:

Reeves’ speech claimed that these figures came instead from “new Treasury analysis I commissioned over the weekend”. Yet Reeves used exactly the same £140bn figure in a lecture she gave in a lecture four months ago. It doesn’t rely on undisclosed data newly dredged from the archives at Horse Guard’s Road.

It’s equally obvious why this “new analysis” performance is useful for the new government: they can argue that they’ve had austerity thrust upon them, having opened their predecessors’ books.

Of course, British politics is littered with big numbers: a £2000 tax bill for every family, £350m a week for the NHS. But the Chancellor’s double rhetorical move (a surprising statistic dramatised as ‘new research’) feels like something particular: the “killer fact” beloved of big British development NGOs of the 2000s and 2010s. I know, because I used to write them.

NGOs have the same media problem as everyone else – the need for an impressive fact to get ‘cut-through’ – but also one that governments don’t face: if an NGO says something, it isn’t actually news, even if it’s interesting. NGO comms departments of the mid-2000s had two standard responses to this problem. First, get a celebrity to say it instead. Preferably Bill Nighy. Second, say that your surprising number is the result of “new research”. Words like “new” or “undisclosed” mean that the big number fits with newsrooms’ (fairly arbitrary) criteria for making something reportable.

This blog’s own Duncan Green originally coined the phrase “killer facts”, after getting media cut-through at a 2000s global summit with the factoid that every cow in the EU gets more subsidy than the income of half the world’s population. Oxfam GB’s Research Department codified “killer facts” comms rules in an (excellent) 2012 guide, prefaced with Duncan’s telling (though correct) sentence: “The right killer fact can have more impact than the whole of a well-researched report.”

The cow stat wasn’t new research, of course, nor claimed as such: it’s simply an arresting fact generated by taking the figure for EU dairy subsidies and realising it comes to about $2 a day. The arresting fact alone can be used for a compelling op-ed. But to make compelling number-crunching into a news story required, well, something “new”. Much like that staple of corporate newsvertising, the “new opinion poll finds”. Eight out of ten cats prefer…but for global poverty.

As a toiler in policy departments of UK development NGOs in the early 2010s, I remember the pressure from well-meaning press officers for a killer fact they could retail to journalists as ‘new research’. Figures for international tax avoidance were particularly susceptible, because they quantified something deliberately invisible: what Jim Henry memorably called “an exercise in night vision…trying to measure…the economic equivalent of an astrophysical black hole”.

Like astrophysical black holes, the numbers got very big. But the fact of making big numbers wasn’t itself problematic. Rather, it was that in the endless internal war between reluctant policy wonks and hard-pressed media officers, our policy briefs’ caveats and provisos usually got stripped away in the press release. And, inevitably, ‘calculation’ segued into ‘research’.

So: three cautionary tales from my own experience of “killer facts”. First, killer fact inflation. Once you’ve put a big number or a shocking ratio on a problem, if you want continued attention then you can’t make it go down, only up. In my area, tackling one particular activity, corporate tax avoidance, eventually became the answer to funding everything: hunger, disease, all public services.

Second, falling back on killer facts, especially if presented as exclusive research, means that the debate becomes about the numbers, not the policy. A lot of the criticism our big numbers got wasn’t fair, or dispassionate. But we spent a huge amount of time defending them.

Worst of all: you start to believe your own big numbers. In our case, an unreasonable focus on the fiscal potential of tackling corporate tax avoidance meant that more fundamental tax policy – including increasing tax rates on wealth and very high incomes – got sidelined for many years. You can see this specific issue in the 2024 Labour Party manifesto, which claims it can fund nearly half of its (admittedly modest) spending promises through tackling ‘tax avoidance’ and the carried interest loophole. Can HMRC’s inspectors really find £6bn down the back of the fiscal sofa? The IFS isn’t alone in thinking it pretty unlikely.

The Chancellor recently delivered the fuller results of Labour’s performative rummaging in the desk drawers at the Treasury. Although this seems more based on real Treasury analysis than special adviser spreadsheets, her opponents have predictably managed to mobilise doubts about dressing up known economic facts as newly discovered black holes – thereby sidestepping real debates about real economic difficulties.

Meanwhile open-source ‘killer facts’ dressed up as research or undisclosed government data conceals policy as economic exigency. From someone who knows, it’s a strategy that can come back to bite.

As a campaigner in the past, I’ve come up with “killer facts” myself and also quietly killed off a few of the sketchier ones.

A common kind of killer fact is the “big number”. Mike lays out the various reasons why we in the NGO world feel that we have to come up with these numbers: in fact I’m about to publish one on the online platform I run (spoiler: it’s a trillion!).

The use of “big numbers” can have virtuous effects, beyond drawing attention to a problem. For example the early NGO estimates of corporate tax avoidance were necessarily quite sketchy because there was so little public data to base them on. But campaigns which used these figures have, among many other things, prompted a gradual increase in the quality and availability of tax data, meaning that newer estimates can be better-informed (and are in some cases larger than those early ones!)

But a basic problem with NGO “big numbers” is that they’re usually not put into global context: that is, what is the bigger number that the “big number” should be compared to, in order to understand its significance?

It’s quite common to see big numbers in the billions of dollars, which is a big deal if one is talking about a set of low-income countries but relatively small potatoes when set against world GDP which is estimated at around $100 trillion.

So the “big number” tactic can play into a common tendency, which exists for other reasons, to look for single-factor solutions to complex global problems.

That said, I don’t have an alternative approach to suggest at this point. One would probably need to rethink the way that political communication happens in our societies.

(Footnote: I’m also a voter in the UK and it depresses me to see a supposedly progressive and reformist government using fiscal “big numbers” in the same slippery, polemical fashion as its predecessor.

There’s a case to be made that NGOs sometimes have no choice but to do this: they’re under-resourced and need to get the attention of decision-makers in the face of vested interests which are usually much more powerful than they are.

But for the government of one of the world’s richest countries, with what is still one of the world’s best-resourced state bureaucracies and an electorate with a high level of education, I just don’t see the excuse.)

Agree entirely with Mike and Diarmid.

Working for HMRC and a trade Union in this

area there was lots of energy and time devoted to reviewing the claims and trying to set them in perspective. There was a sense of frustration that the debate and analysis was losing perspective, with well meaning people apparently believing in the pot of gold at the end of some rainbow.

Notional gains for poor nations of a few $per head are obviously better than nothing but they seem to become elevated to fundamental improvements. I also worried that there was an unintended consequence that poor nations just needed MNC taxes to jump forwards and do nothing else.

To clarify, Iain, I do think there’s a global pot of gold to be had from reforming international corporate taxation. The estimates I know of suggest that it’s in the hundreds of billions of dollars (depending on definitions etc), a massive sum by any standard that fully justifies the attention given to it.

Where I think the big numbers can be problematic, and where maybe we agree, is when people make optimistic inferences about individual countries from these global figures without reflecting that this additional revenue would not be evenly distributed around the world i.e. most of it would be attributable to high- and bigger middle-income countries, because that’s where most of the corporate investment is, and for some of these countries (e.g. the UK), the potential gains would be relatively small in proportion to total revenues.

That said, I have seen cases in LMICs where the tax at stake appears to be in the tens of millions. So while CIT reform should certainly not be portrayed as a panacea for poverty, there are potentially significant revenue gains to be had even in relatively small economies.

Exactly this: to stick with this blog’s theme of power, the international tax system is not an autonomous machine that delivers revenue to countries mechanically; it’s a set of legal tools that enable or constrain revenue authorities, if the political will exists, to challenge particular “bad deals” involving particular corporate taxpayers. Mines in Mongolia, Apple in the EU. As Diarmid says, the sums involved are sometimes transformative for small countries’ public purses. Which is also my larger, non-tax point: big aggregate numbers are politically seductive, and possibly politically useful; but they obscure the qualitative value of policy changes: value which probably isn’t quantifiable in advance, and which is easily dismissed (as with BEPS) if the overall quantitative impact isn’t what the killer fact promised.